ACA silver coverage would cost them about $1450 a month. With a $950 a month subsidy, that nets out to $400 a month. Not bad!

But the real question: Do you go to the doctor a lot? Any chronic illness (like diabetes)? Many prescriptions? No, no, no.

Have you considered a Health Savings Account (HSA)?

At one time the husband had a Flexible Spending Account (FSA) through his employer. FSA is “Use it or lose it” with only a small amount that can carry over from year to year.With HSA, what you don’t use is YOURS TO KEEP. And you can save/invest it just like an IRA.

The key benefit

Money goes Tax-Deductible IN, Tax-Free OUT for medical purposes (even if they aren’t covered by your major medical plan). At retirement age, the money can be used for any purpose just like an IRA.HSA is a Medical IRA. It is SUPERIOR to the typical IRA. Why? Typical IRAs only provide a one-sided tax benefit. Either they are Tax-Deductible IN (traditional IRA for those who qualify) or Tax-Free OUT (Roth IRA, but only when the account has been established at least 5 years AND the client is over 59 1/2).

HSA has 3 tax advantages...

1) Tax-Deductible IN (regardless of income levels that would disqualify typical IRAs) and2) Tax-Free OUT (immediately, no 5 year wait like Roth IRAs) and

3) Qualified medical expense acts as a Get-out-of-jail-free-card for your money. (Now or later)

For item 3: You can use it right away, or use it to make a tax-free withdrawal years into the future. AND recognized medical use includes things like premiums for Long Term Care insurance, mileage expense and lodging for medical, orthodontia, vision, etc.

But to get these benefits, you need a High-Deductible Health Plan (HDHP). Conveniently, these usually have HSA somewhere in their name. Unfortunately, Covered California usually only has 1 or 2 HDHP choices in its lineup.

The cost?

In this case, the bronze 60 HSA-compatible plan costs $4.30 per month... for the whole family.They can take a PORTION of their COBRA premium and stash it into their HSA. With their HSA, they can see any doctor. (One of the big bugaboos for ACA has been the restricted doctor networks.) If a doctor’s visit costs $100 or so (cash discount available for the asking), they come out ahead even if their usage is 20x what it has ever been. They will save up the whole ANNUAL deductible for their bronze plan in a matter of months.

Typical story. High cost COBRA: $2000/mo. Lower cost individual plan: $1450/mo. Net ACA cost: $400/mo. or $4.30/mo and SAVE THE DIFFERENCE.

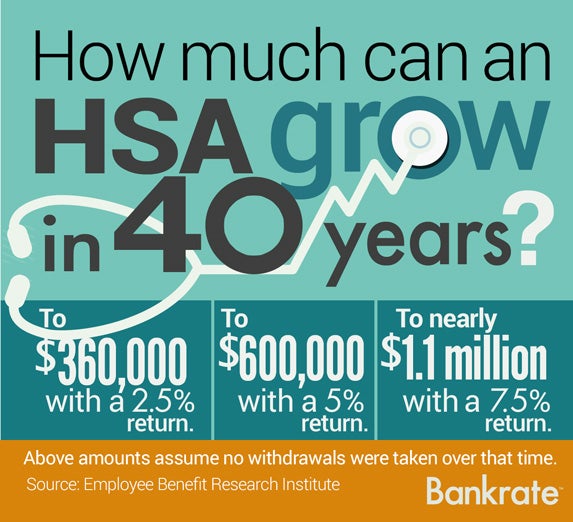

BTW, I have clients who have used HSA for over 10 years. Some have balance of $50,000 or more. What is the long-term potential?

No comments:

Post a Comment